Payday Loans in Canada: What to Know Before You Borrow

Payday loans are short-term loans designed to cover urgent expenses until your next paycheque. In Canada, rules and cost caps can vary by province, which is why borrowers should always check local guidance before applying. This page breaks down how payday loans work nationwide, what lenders typically require, how repayment works, and what alternatives may help you avoid high borrowing costs.

Smart move: review total repayment amount and due date before accepting any offer.

Why “Payday Loans Canada” isn’t one-size-fits-all

People often search “payday loans Canada” expecting one universal answer. The reality is more nuanced. Payday lending in Canada operates under federal and provincial frameworks, meaning rules and caps can differ by region. Some provinces have stronger restrictions, while others may have different requirements for licensing, disclosure, and borrower protections.

That’s why we organize guidance by province and keep our content focused on what borrowers actually need: the repayment timeline, the total cost, what lenders typically ask for, and practical ways to reduce risk. If you want the most relevant guidance fast, start here: Payday Loans by Province →

What a payday loan is (and what it isn’t)

A payday loan is generally a short-term loan meant to bridge a financial gap until your next payday. It’s not designed for long-term borrowing or ongoing cash flow problems. If you need months to repay, an installment loan or alternative solution may be more appropriate.

Payday loans are often used for urgent, time-sensitive expenses such as:

- Emergency car repairs

- Overdue utility bills

- Unexpected medical or household costs

- Short-term gaps before payday

However, because they’re meant to be repaid quickly, they can create pressure if the borrower’s budget can’t absorb the repayment. This is why we emphasize readiness and cost clarity.

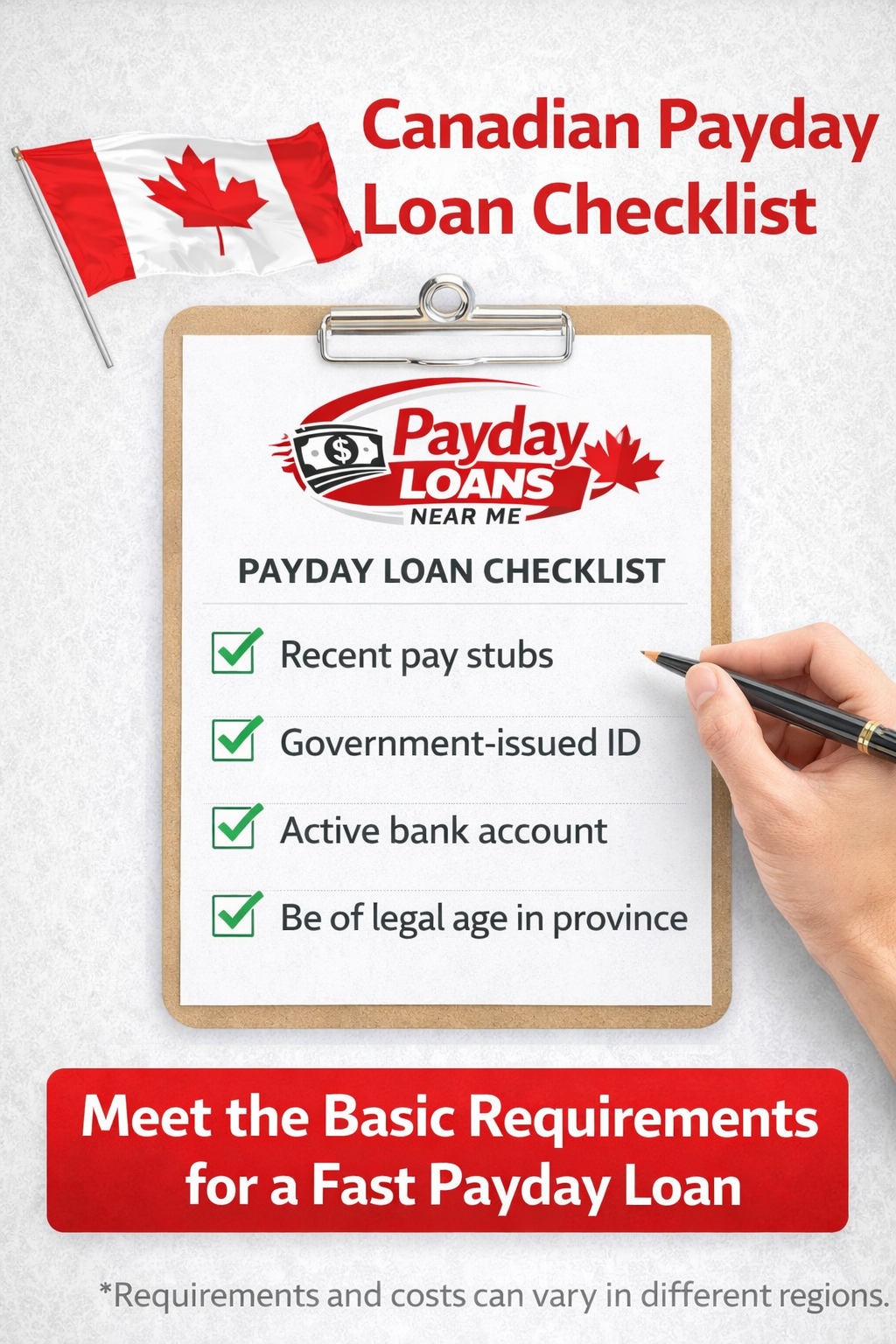

Typical eligibility requirements in Canada

Exact requirements vary by lender and province, but many lenders commonly request:

- Proof of income (employment or other income source)

- Active bank account details

- Government-issued identification

- Valid contact information

- Residency in a Canadian province/territory

Some lenders may also require additional verification. If you’re applying online, ensure you are using a secure connection and avoid submitting sensitive information on unfamiliar sites. If you want an overview of the full process, see: How It Works →

Costs: focus on “total repayment” and due date

Payday loans may include fees that can add up quickly. Instead of only looking at the amount you receive, focus on the full amount you must repay and the date it’s due. A payday loan is meant to be short-term, which means you need a realistic plan to repay it without missing essentials like rent or groceries.

Before accepting any offer, confirm:

- The total repayment amount (loan + fees)

- The repayment date and payment method

- Any fees for late payment or extension

- Whether early repayment changes anything

For an in-depth breakdown, visit: Payday Loan Rates & Fees →

Province-based differences (why your location matters)

Canadian borrowers should be aware that payday loan rules are often enforced at the provincial level. This can affect:

- Maximum fees or cost caps

- Disclosure requirements

- Lender licensing rules

- Borrower protections and complaint pathways

Instead of guessing, use our province hub to find guidance relevant to your area: Payday Loans by Province →

A practical checklist before borrowing

We want this guide to be genuinely useful — not just “SEO content.” If you’re considering a payday loan, pause and run through this checklist:

- Can I repay on the due date without borrowing again?

- Do I understand the total repayment amount?

- Have I checked alternatives first?

- Have I reviewed the lender’s terms and disclosures?

- Will repayment disrupt essentials like rent, food, or utilities?

If you’re unsure about any of the above, start with alternatives: Alternatives to Payday Loans →

If you’re ready to apply

If you’ve reviewed the costs and you’re confident you can repay on time, you can continue to the application flow. We recommend applying only when your budget supports repayment.

Apply Online → Review the Process